Big Miners Set to Become Juniors’ Primary Funder

Many explorers and developers are yet to see meaningful share price moves

Cashed up producers are set to become a major financier to the struggling junior sector, according to Cupel Advisory Corp’s Neil Adshead.

Adshead told the Mining Forum Europe in Zurich this week that while record gold prices were trickling through to the share prices of the producers, the junior end of town was still doing it tough.

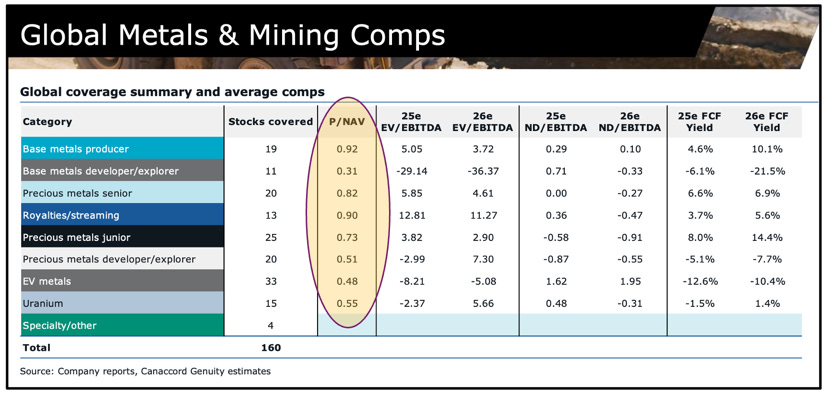

He pointed to a recent Canaccord Genuity report, which showed the juniors under its coverage were trading at a price to net asset value of below one.

“It's impossible to argue this sector is overvalued in any capacity,” Adshead said.

“Now, some stocks trade above the P/NAV of one, but as a sector, it is still really cheap despite the metal prices, so it's a pretty attractive sector.

‘You kind of wonder why there's not more money coming into especially the juniors.”

Selling the dream

Success stories like Great Bear Resources don’t come along very often but can be enough to attract money into the broader sector.

“It's kind of selling the dream – the amazing returns you can make is what attracts people into this, especially into the juniors,” Adshead said.

Adshead said investing in junior mining could be compared to gambling, which was driven by emotions including the thrill of the hunt, greed and fear of missing out.

The global gambling sector is worth US$1.1 trillion and is forecast to grow to US$1.4 trillion by 2030.

“If you think of junior mining as a form of gambling, how can we direct some of that gambling money into the juniors, into taking a wager?” Adshead said.

“Maybe the juniors have got to think about exploration as a form of gambling and sort of sell those emotions. You've got to trigger those emotions for especially the retail audience to give them some money.

“You've got to appeal to this sort of greed gene, this desire to explore the thrill of the hunt.”

Adshead said the explorers weren’t doing a good job of appealing to gamblers.

“There's something lacking in the pitches, so maybe there's some juniors watching this on the video – and I'm more than happy to have this discussion with people later as to maybe how they can improve how they how they actually pitch their stories to the gamblers of the world who are essentially investing over US$1 trillion and essentially losing at the moment to the official gambling industry,” he said.

He also suggested Australians were much bigger gamblers than Canadians, which could be one reason why liquidity was better on the ASX than the TSX.

Emergence of the ‘super junior’?

As a capital allocator, Adshead hears lots of pitches and advises companies to match their business plan to their capitalisation.

“I've seen this from attending thousands of meetings, and now I can see this quite quickly, but quite often the business plan scope and the capitalisation are mismatched,” he said.

“Now, when they're ideal, it's basically what are you trying to do and have you got enough money to do it? It's essentially, is the business plan properly capitalised?”

Adshead likes the concept of what he calls a “super junior”.

He said Ivanhoe Mines (TSX: IVN) has historically been a good example of a super junior.

“Robert Friedland's got four massive discoveries assigned to him, and people say, ‘oh, there's so much luck’.

“Is Robert Friedland lucky? I don't think Robert Friedland's lucky. I think Robert Friedland’s a fantastic financier who can raise enough money, hire the best geologists in the world, pick up massive pieces of ground, and explore them for 10 years, and so few juniors can do that,” Adshead said.

“What I mean by a super junior is maybe a junior that's got at least US$100 million on the balance sheet and a five-year outlook.

“So I'd love to see somebody come along with the super junior concept.”

Majors outsourcing exploration

The large companies, for the most part, are not spending as much on exploration as they once did.

Adshead worked for Placer Dome in the 1990s as a geologist and said it used to have a huge exploration budget and 250 people in the exploration team.

“The big boys say they're spending a lot of money, but not a lot of it is on grassroots, a lot of it is brownfields these days,” he said.

“If you look at some of the big boys today, they've got much reduced teams and they outsource a lot of it. They option projects and let the other junior do the work, or they completely outsource it.”

With gold trading at more than US$3100 an ounce, the large producers are generating huge margins.

“We're seeing quite a lot of the corporates sitting on hundreds of millions of dollars and they're starting to give money to good groups, giving them sufficient money, enough money to say, ‘right, we think you guys are really good, you've got a good piece of ground, go explore’,” Adshead said.

Agnico Eagle Mines (TSX/NYSE: AEM) has been particularly active in that regard in recent months, making or increasing investments in Rupert Resources (TSX: RUP), Collective Mining (TSX: CNL), Cartier Resources (TSXV: ECR), Ongold Resources (TSXV: ONAU) and ATEX Resources (TSXV: ATX).

B2Gold (TSX: BTO) has invested in Snowline Gold (TSXV: SGD) and Founders Metals (TSXV: FDR), while Kinross Gold (TSX: K) is invested in Relevant Gold (TSXV: RGC).

“So there's lots of companies doing that right now, and I think it's an increasing source of capital for junior explorers going forward,” Adshead.

Adshead is working for Centerra Gold (TSX: CG) on a part-time basis as essentially an in-house fund manager.

“Centerra has US$25 million to invest, basically buying 10% in various juniors, and they really do want to invest in early stage gold explorers,” he said.

Centerra has recently invested in Headwater Gold (CSE: HWG), Dryden Gold Corp (TSXV: DRY) and Kenorland Minerals (TSXV: KLD), the latter of which he said had the potential to be a super junior.