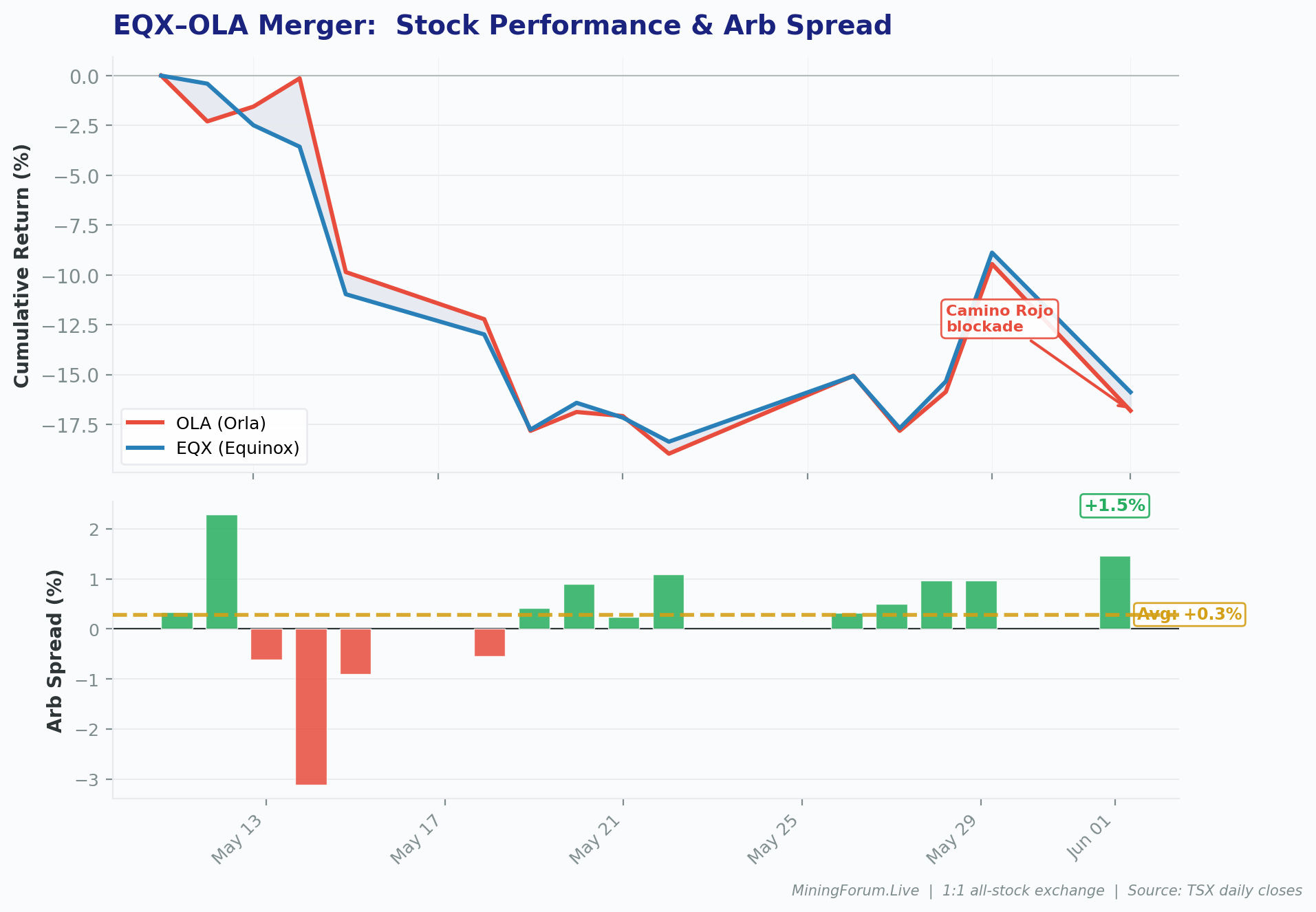

Camino Rojo Blockade Tests the EQX-OLA Merger Spread

A wildcat work stoppage at Orla’s flagship mine puts the 1:1 all-stock deal with Equinox under the microscope.

Orla Mining disclosed this morning that unionized workers at its Camino Rojo mine in Zacatecas, Mexico, launched an illegal work stoppage and blockade, halting mining operations. The dispute centers on two payments: a productivity bonus still under negotiation, and a profit-sharing entitlement (PTU) that Orla says it has already paid at the statutory maximum under Mexican law.

The stoppage has not followed the procedures required to constitute a legal strike (no strike notice was filed). A conciliation meeting with Mexico’s Department of Federal Labor is scheduled for tomorrow, June 2.

Orla’s stock dropped 8.1% on the day. Equinox Gold, which is acquiring Orla in a 1:1 all-stock merger, fell 7.7%.

What the Spread Signals

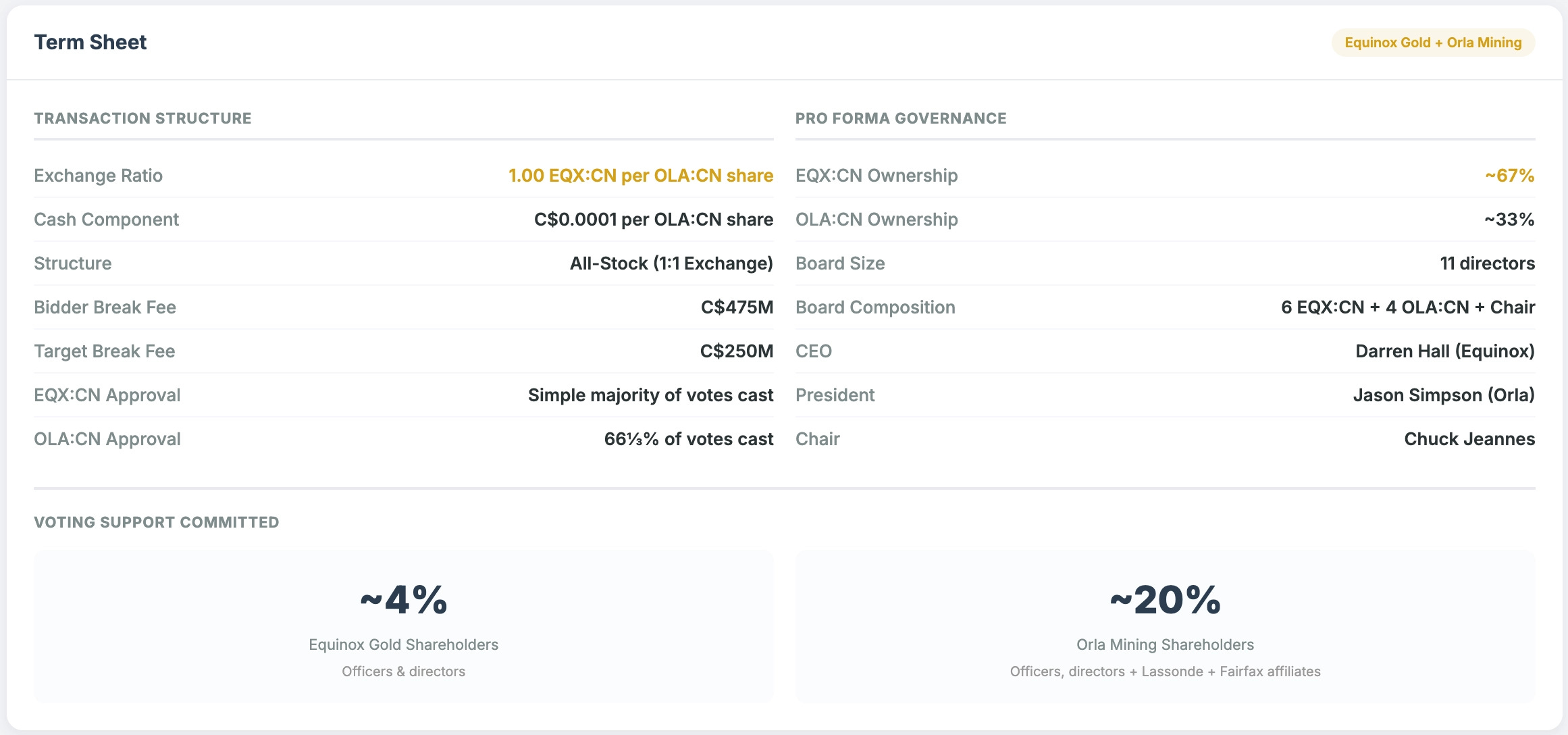

The EQX-OLA deal is structured as a 1:1 share exchange. In a perfectly priced deal with zero completion risk, the two stocks should trade at parity. Any divergence is the merger arbitrage spread: the market’s real-time verdict on whether the deal will close at the agreed terms.

At the announcement, the spread was negligible (+0.3%). Over the past three weeks, it has drifted wider, settling at +1.0% by last Friday. Today it jumped to +1.5% — the widest level in the dataset.

A positive spread means Orla trades below its deal-implied value. In plain terms: the market thinks there is a small but growing probability that OLA shareholders receive less than one full EQX share of value at close, whether through deal renegotiation, a failed vote, or an outright termination.

Gold Price Impact

Gold closed at $4,494/oz today, up 0.2%. Silver was up 0.4%. Both stocks fell nearly 8% on a day the underlying commodity was flat to positive.

That confirms Camino Rojo-specific operational risk is repricing both sides of the deal; Orla because it’s their mine, Equinox because they’re about to own it.

Scenarios

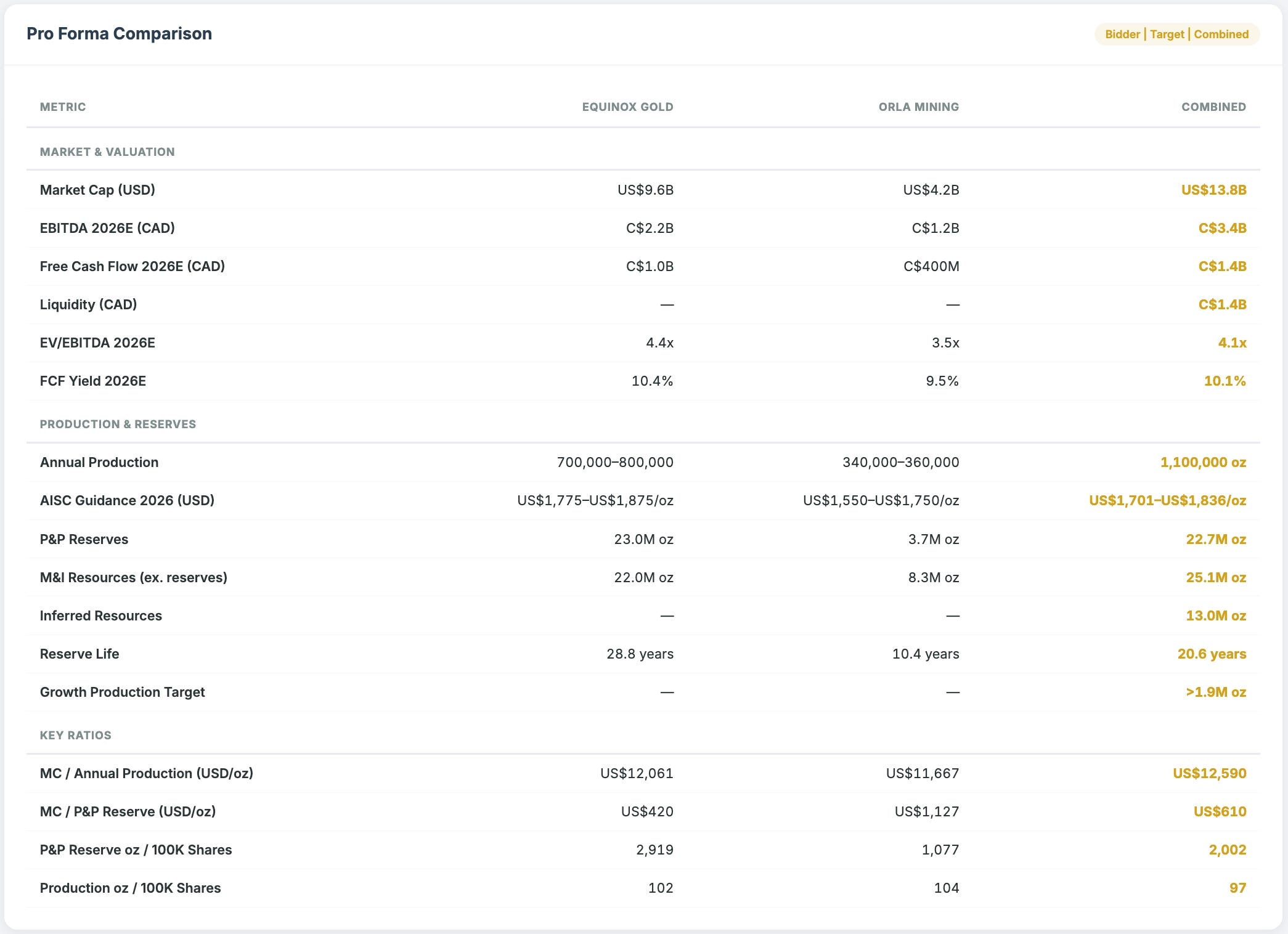

Camino Rojo is a load-bearing piece of this transaction. It’s Orla’s primary producing asset and a principal reason Equinox agreed to a 1:1 ratio, valuing Orla at effective parity. So, there are three possible scenarios from here:

Quick resolution (days). The conciliation meeting produces a settlement, workers return, and production resumes. The spread compresses back toward 1%, and both sides proceed to a shareholder vote. This is the base case, especially since wildcat PTU disputes at Mexican mines are not uncommon during profit-sharing season and typically resolve within days.

Prolonged stoppage (weeks). Orla is forced to revise production guidance. The 1:1 ratio starts to look generous to Orla shareholders (whose standalone asset is impaired) and expensive to Equinox shareholders (who are absorbing a disrupted mine). Internal pressure builds on Equinox’s board to seek a ratio adjustment. The spread widens past 3%.

Structural labor problem. If the blockade reveals deeper union dynamics, jurisdictional disputes, political entanglements, and the risk of repeat stoppages, it could trigger a Material Adverse Effect review under the merger agreement. MAE claims on labor disputes are notoriously hard to sustain, but the threat alone could delay the closing timeline and push the spread toward 5%+.

What to Watch

The arb spread is the market’s composite risk score for this deal. At +1.5%, the verdict is clear: this is a bump, not a dealbreaker. But the direction is what matters. The spread has moved in one direction (wider) for three straight weeks, and today’s Camino Rojo news accelerated the trend.

If the conciliation meeting tomorrow produces a framework for resolution, expect the spread to stabilize. If it doesn’t, the next data point is whether Orla updates production guidance and how Equinox responds.

The Denver Gold Group does not provide investment advice. This analysis is for informational purposes only and reflects the opinion of the author based on publicly available data as of June 1, 2026.