Mining Forum Europe 2026: Follow the Capex

How issuers are raising and spending cash for project builds.

At any stage of the mining cycle, the capex line is where the truth is most clearly reflected. Management can talk about discipline and per-share metrics all day, but what they spend on rock in the ground and infrastructure above ground is the final measure of what the industry's future will look like, and how investors will be compensated. Over three days at Mining Forum Europe 2026, the question that mattered was how these companies actually plan to deploy the cash that gold, just below $5,000, is handing them, even after suffering the hit from catapulting oil prices. What follows is what corporate presenters said, organized around the capex patterns that emerged.

The capex wave is real, but differently shaped than in 2009-2012

A capex wave is developing, even if it looks very restrained in detail. Counting only the builds that are either funded or in execution among the 63 of 70 companies that presented, the aggregate capital intent on the floor was in the range of $10 to $12 billion, spread over the next three to four years. The top of that stack is dominated by a handful of large projects that now have both the balance sheet and the permits to move forward.

What makes this project cohort different from the 2010 to 2012 set is that each project has been right-sized thoroughly before the trucks arrived. Pan American Silver's La Colorada expansion is, arguably, the cleanest illustration. In the prior design, the capex line was close to $3 billion, and the mine plan targeted maximum throughput. In the version management presented this year, the capex was $1.9B, the project is sized to mine the high-grade structures within the skarn rather than maximum tons, and the entire program is funded from existing cash and ongoing cash flow while the company continues to return roughly $100 million per quarter to shareholders through dividends and buybacks. That is a very different capital posture from the last bull market, and versions of it turned up in almost every producer presentation on the floor.

Right-sizing is the dominant capex discipline

Vista Gold‘s [$324.68M, $2.24] Mount Todd story was the most straightforward example of what right-sizing looks like in practice. The prior feasibility study estimated capex of over $1 billion for a 50,000-ton-per-day operation. The version presented this year cuts the build to 15,000 tons per day and $425M of capex, achieved mostly by raising the cutoff grade from 0.35 to 0.5 grams per ton and redesigning the pit. The economics at $3,300 gold now show a $2.2B NPV and a close-to-45 % IRR, with a doubling of the 15,000 tpd base left as future optionality rather than a day-one commitment. The old version was unfinanceable for a junior. The new version is financeable and preserves upside, particularly by giving senior miners a way to test the project before buying it and creating a market expectation for a full-size endeavor.

The same playbook turned up under different labels throughout the event. Paramount [$150.03M, $1.79] redesigned Grassy Mountain as an underground mine rather than an open pit, and is waiting for the DFS refresh before putting a new capex number around it. Aura Minerals [$9.14B, $109.14] has institutionalized the discipline as a build strategy, with Almas built for $75M and Borborema built on a comparably small-capex basis, each then expanded with internally generated cash once the initial plant had paid itself down. Aura’s own management framed it plainly, saying they build fast, minimize capex, get payback quickly, and then expand using the proceeds rather than tapping the market for equity or debt. Tesoro‘s [$129.36M, $0.72] El Zorro in Chile is scoped at $250M to $350M largely because the company has resolved water (desalination brine) and power through early MOUs rather than building standalone infrastructure. In almost every case, the capex number looks smaller than the equivalent project would have looked a decade ago, not because the assets are smaller but because management is deliberately constraining the first-phase build.

Brownfield is where the cheap capex lives

If right-sizing is the discipline of choice for new builds, brownfield acquisition remains a cheat code that several companies are exploiting. The best example was West Red Lake [$341.75M, $0.83], which acquired the Madsen mine out of bankruptcy for roughly $6M after the previous operator (Pure Gold) had sunk about $350M into the build. The company is now spending its capital on underground definition drilling (200,000 meters at six-meter centers over the last 18 months) and satellite development at Fork and Rowan, with the existing 800 to 1,500-ton-per-day Madsen mill as the central hub. Nothing in the program resembles a greenfield capex wave. It is essentially an exploration and tie-in program sitting on someone else’s sunk cost.

Discovery [$6.47B, $7.99], Orla and Minera Alamos [$531.18M, $4.92] all told variations of the same story. Discovery acquired the Porcupine complex from Newmont for $200M in cash and $75M in equity, and announced on March 2, 2026 the acquisition of Glencore’s Kidd operations in Timmins (KidMed site and tailings facility) as processing capacity for expansion. Orla bought Musselwhite from Newmont for $850M in Q1 2025 and is running the portfolio alongside South Railroad and Camino Rojo under a single capital plan. Minera Alamos acquired the Pan mine from Equinox Gold [$12.32B, $15.63] at the beginning of October 2025, and is building Copperstone and Cerro de Oro around it as a low-capex multi-asset Mexican and US business aiming for roughly 150,000 ounces of production on about $130M of capital. Maritana [$176.22M, $0.68] in Western Australia (the former Horizon Minerals, renamed the week of the forum) is refurbishing the Black Swan nickel plant into a gold operation for $160M, a capex figure the company claims is about half that of a new build and roughly twelve months faster. The pattern across all of these is that capex per ounce on brownfield sits well below the per-ounce capex on any new greenfield pit in the same jurisdiction.

Low capital-intensity mine plans are being deliberately favored

Several of the development stories presented at the forum were structured specifically to minimize capital intensity in the first phase, with the implicit argument that in this commodity price environment simpler and faster is worth more than bigger and better. The set below was striking for how low some of the numbers are.

Q Gold Resources [$38.70M, $0.25], Quartz Mountain (Oregon): PEA released one week before the forum, $290M initial capex for 135,000 ounces per year, 1.8 year payback, 55% IRR at $3,265 gold. Heap leach for the first five years, then conventional milling.

Amex Exploration [$534.26M, $3.78], Perron (Quebec): $193.9M Phase 1 capex, with a $50M bulk sample program the company expects to largely self-fund through pre-production gold and toll milling arrangements. Post-tax 78.8% IRR, even at $2,500 gold; 0.6-year payback at higher prices.

Lahontan Gold [$113.02M, $0.32] (Nevada): $135M total capex, 18-month payback at $4,000 gold, with Phase 1 deliberately scoped under a 640-acre EA rather than the full EIS to compress permitting by about a year.

Liberty Gold [$594.85M, $1.13], Black Pine (Idaho): $327M capex, sub-two-year payback at $3,000 gold, with the project on a FAST 41 critical minerals permit schedule that sets a federal record of decision deadline of January 5, 2029.

Contango [$753.84M, $24.71], Manh Choh (Alaska): The original DSO build cost about $70M because the ore is trucked to Fort Knox for tolling rather than processed on site. This model is now being extended to Lucky Shot, which Contango has scoped as a DSO into Fort Knox, with roughly $21M in feasibility work this year and $35M the following year.

Rio2 [$1.12B, $2.13], Phoenix Gold / Fenix (Chile): Construction finished in January 2026, and the mine is now in production. Management stated on stage that the company does not intend to pursue any further capital raises, financings, or borrowings, and that the 80,000-ton-per-day expansion PFS is targeted for release at the end of Q1 2026.

The common thread among these names is that grade, location, or metallurgy allows the first-phase mine plan to avoid a conventional large mill. When management can credibly argue that an operating asset can be built for under $400M and repaid within 24 months at current prices, the financing equation changes completely, and the equity story can carry itself through construction without a mid-build dilution event.

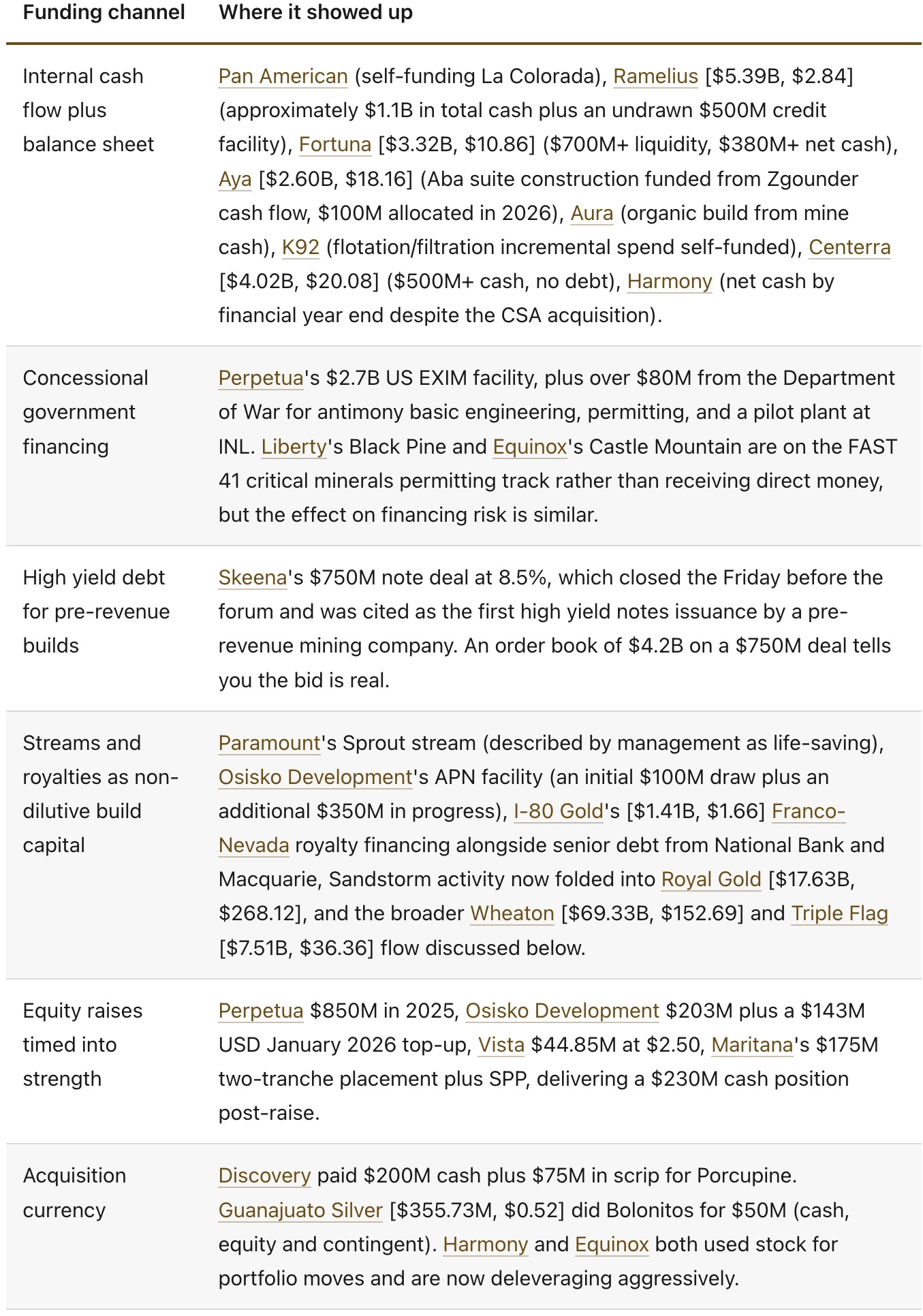

How the capex is actually getting funded

Funding is where the cycle has moved the most since 2011. Almost nobody at the forum is relying primarily on the traditional senior bank syndicate to build their mine. The mix now looks like this:

The most important aspect of this table is the absence of a single dominant capex funding model. Where once the sequence was equity raise, then senior bank term loan, then construction drawdown, the 2026 mix is a blended stack that takes liquidity from wherever it is cheapest and leaves the equity line as a last resort rather than a first stop.

What the streamers are signaling

To triangulate on the capex wave, listen to the people writing the non-dilutive checks. Wheaton Precious Metals’ headline transaction was the $4.43B BHP Antamina stream, completed in February 2026 and described by management as the largest precious metals streaming transaction ever. Wheaton has invested nearly $19 billion in streams since inception and is forecasting more than $10 billion in operating cash flow through 2028 at current metal prices. Royal Gold deployed $5.3B of capital over a six-month period through the Sandstorm Gold and Horizon Copper acquisitions (together the largest corporate acquisition in the sector’s history), along with a $1B gold stream on a First Quantum-operated mine in Zambia and an equity investment in the Winsa copper project in Ecuador. Triple Flag deployed $350M into new streams over the last year and expects its production profile to grow to the 140,000 to 150,000 gold-equivalent ounce range by 2030.

Three messages came through clearly from the streamer panels. The first is that the pipeline is not the constraint. Each of the three had liquidity above $1 billion at year's end and described the 2026 deal calendar as the busiest they had seen. The second is that counterparty capex is genuinely large, and streamers are absorbing a meaningful share of the financing role that banks used to play, particularly for development and expansion situations at producers who do not want to issue equity at current multiples. The third is that pricing discipline is still in place. Each of the three referenced deal sizes in the $300M to $500M range is the sweet spot, with hurdle returns sustained at 8 to 10 percent on an initial basis and margins maintained above 80 percent. When streamers say they are not stretching on price, they are also saying that miners are not so desperate for capital that they will accept bad terms. Both sides of the market are behaving.

Payback math defers hedging demand

The most underreported piece of the capex story is the payback math that companies were quoting. At current prices, the projects going forward are not marginal. A handful of illustrative figures from the floor:

Amex quoted a 0.6-year payback at $3,500 gold on the Perron Phase 1 build and a 78.8% post-tax IRR at $2,500 gold with a 0.6-year payback.

Q Gold quoted a 1.8-year payback and a 55% IRR at $3,265 gold on Quartz Mountain.

Tesoro quoted an 85% IRR and an NPV well in excess of $1 billion on El Zorro at $3,950 gold, scaling to a ~$2B NPV and a triple-digit IRR at higher prices.

Lahontan described an 18-month payback at $4,000 gold on a $135M build.

Liberty showed a sub-two-year payback at $3,000 gold on Black Pine, with $125M of NPV sensitivity per $100 move in gold.

Aura quoted a 64% expected rate of return on Almas at sub-$2,000 gold and an IRR over 80% on Borborema at $2,600 gold.

Newcore Gold [$137.32M, $0.48] ran Enchi at $3,000 gold and showed a post-tax NPV of $970M with a half-year payback.

Teams that can quote numbers like those have no reason to hedge future production into the build, which is why few people on the floor were discussing price protection. Indeed, investors are still asking for full exposure to the gold price rather than safety first. The producers with operating mines do not want to cap their upside, and the developers do not need to cap anything because the paybacks clear well inside any realistic downside scenario. That is a very different mood from the one this industry was in 20 years ago.

Capex inflation is real, but it is being absorbed

The one area where candor was in shorter supply was labor and equipment inflation. Almost every team acknowledged it in passing. Skeena‘s management flagged that the original 2023 feasibility all-in sustaining cost of under $550 per ounce would likely reset to the $750 to $800 range by the time construction is complete. Ramelius described a cost program targeting approximately $2,000 per ounce all-in sustaining in Australian dollar terms, equivalent to roughly $1,400 US. Nobody claimed cost inflation was behind them, but nobody described it as a project-killing risk either. The strategy for absorbing it is almost identical across the group: raise the cutoff grade, mine a narrower and higher-grade portion of the resource, preserve expansion optionality for later, and keep the first build modular. That is a sensible response to a cost environment that has not yet stabilized, and it is part of why capex numbers look smaller than they otherwise would.

Implications for allocation

Pulling the pieces together, the capex picture coming out of Mining Forum Europe 2026 is not the 2011 capex picture, and the differences matter to investors. Capex is larger in aggregate than it was three years ago, but the projects carrying most of the dollars have been right-sized, phased and pre-funded in ways that make them much harder to blow up. The dominant financing model has shifted away from bank debt toward a layered stack of internal cash, streams, royalties, high yield, concessional government support, and equity reserved for the cleanest opportunities.

Brownfield acquisitions are now the cheapest capex a mining company can deploy, and the set of majors willing to sell non-core assets has made that an actual strategy rather than an aspiration. The streamers have more capital than they know what to do with, which will keep the non-dilutive funding channel open even if the equity window narrows. And exploration spending is rising across almost every name, which is the closest thing on the floor to a shared statement of confidence in the cycle.

For a capital allocator working in this sector, the corporate presenters at MFE 2026 pointed toward a handful of clear preferences. Producers that are self-funding growth while returning cash look very well positioned, and Ramelius, Pan American, Fortuna, Aya, K92, and Orla are the names that warrant closer work. Developers with modular mine plans, short paybacks, and a non-dilutive funding component look more investible than the traditional large-build stories, and Q Gold, Amex, Liberty, Lahontan, Tesoro, and Rio2 (just in production) fit that profile. Operators of brownfield acquisitions that are now turning into hub-and-spoke systems are the quiet compounders of the cohort, with West Red Lake, Maritana, Minera Alamos, and Discovery all fitting the description. The large, genuinely capital-intensive builds (Perpetua, Greatland, Harmony‘s Eva Copper, Osisko Development) will be defined by execution rather than financing, and construction metrics should come into view before sizing decisions. Streamers look structurally well-positioned to keep compounding through the cycle, with Wheaton, Royal Gold, and Triple Flag all describing deal pipelines that the equity market has not fully priced in. IAMGOLD [$11.21B, $19.25] sits in the same category, where execution reporting will matter more than model optionality.

None of this is a forecast about the gold price or any particular stock price, and none of it is a case that the cycle has to end well or early. It is simply a reading of what the companies themselves are doing with the cash. On that evidence, the capex wave finally arriving looks more disciplined than any prior wave in this industry’s recent history, and the companies deploying it well should continue to compound for some time before the industry starts behaving the way industries at cycle peaks always eventually behave.

Sources: company presentations and associated Q&A from Mining Forum Europe 2026. Company links point to presentation recordings. Market capitalization and share price figures in square brackets reflect the April 17, 2026, close in the currency of primary listing (USD unless otherwise noted). Numbers cited in the body reflect what management stated on stage and on panels; please do your own work before sizing a position. It’s a large volume of presentations in a short time frame - mistakes can be made!

Notices

We have taken every care to ensure this data is accurate, but Denver Gold Group cannot accept responsibility for any sourcing variances, mistakes, errors, or omissions, or for any action taken in reliance on it. Use of this data is governed by Denver Gold Group’s Terms of Use.

INVESTMENT ADVICE - NO OFFER OR RECOMMENDATION

The Denver Gold Group and the information and materials presented on this Web site are not, and shall not be construed as, making any recommendation or providing any investment or other advice with respect to the purchase, sale, or other disposition of any regulated gold related products or any other regulated products, securities or investments, including, without limitation, any advice to the effect that any gold-related transaction is appropriate or suitable for any investment objective or financial situation of a prospective investor. A decision to invest in any regulated gold-related products or any other regulated products, securities, or investments should not be made in reliance on any of the information or materials presented or obtained from the Denver Gold Group. Before making any investment decision, prospective investors should seek advice from their financial, legal, tax, and accounting advisers, take into account their individual financial needs and circumstances, and carefully consider the risks associated with such investment decisions.