Scale, Discipline, and Growth: Inside the Royalty Playbook

At Mining Forum Americas 2025, nine royalty and streaming firms reveal how portfolio design, geography, and growth pipelines will separate winners from laggards.

The presentations at Mining Forum Americas 2025 from Wheaton Precious Metals [WPM:CN, $107.71, $48.4B], Franco-Nevada Corporation [FNV:CN, $203.81, $39.3B], Royal Gold, Inc. [RGLD:US, $195.43, $12.9B], OR Royalties Inc. [OR:CN, $36.91, $6.9B], Gold Royalty Corp. [GROY:US, $3.75, $640.2M], EMX Royalty Inc. [EMX:US, $4.20, $464.9M], and Empress Royalty Corp [EMPR:CN, $0.65, $82.3M] offer a detailed look into the strategies that are shaping the royalty business. While all the companies share a basic business model, their presentations reveal distinct philosophies on scale, risk, growth, and capital allocation.

Scale & Strategy: Defining the Path to Value Creation

The companies' market capitalizations are reflected in their distinct strategic narratives, from large-cap leaders to smaller consolidators.

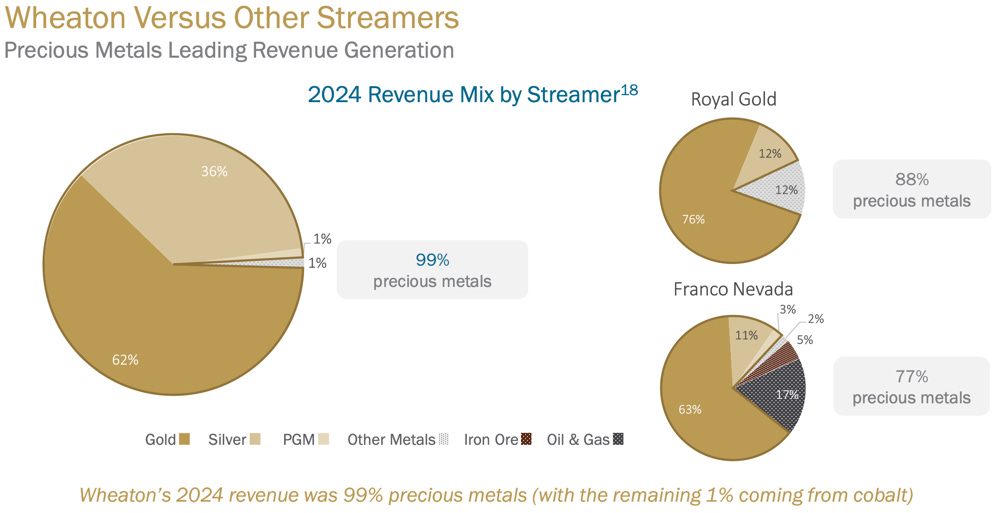

• Wheaton Precious Metals [$48.4B]: As the largest player, Wheaton's narrative is one of quality over quantity: "I've never wanted to be the biggest. I've always wanted to be the best," said CEO Randy Smallwood. This philosophy manifests in a "100% streaming model" and deep caution towards corporate M&A, where acquiring peers risks inheriting "skeletons in the closet". Instead, Wheaton acts as a strategic partner in asset-level transactions, like its recent stream to help finance the acquisition of the Hemlo mine from Barrick [B:US, $29.03, $49.5B].

• Franco-Nevada [$39.3B]: Franco-Nevada's strategy is defined by a culture of ownership and a mantra to "grow profitably," not for growth's sake. The company is comfortable letting cash build if high-quality deals are not available, demonstrating a patient approach focused on generating a high return on invested capital.

• Royal Gold [$12.8B]: Royal Gold's narrative is dominated by its "transformational" acquisition of Sandstorm Gold Royalties [SSL:CN, $12.15, $3.6B] and Horizon Copper. The company is in an integration phase, with the deal's success benchmarked against developing key acquired assets like Mara and Plat Reef.

• OR Royalties [$6.9B]: As a mid-tier player, OR Royalties presents a narrative of highly disciplined growth. With a "very high" appetite for deals, it stresses it will not do "0% IRR deals in Africa" to compete, often ending up in "second place" on transactions—a testament to its discipline.

• Gold Royalty Corp. [$640.2M]: Gold Royalty's narrative is one of an aggressive consolidator aiming to create a new "mid-tier champion" to fill a landscape it believes will soon be "vacant". Its unique four-platform strategy—M&A, royalty financing, third-party acquisitions, and organic "royalty generation"—is designed to build a portfolio at a low cost base.

• EMX Royalty [$464.9M] & Elemental Altus Royalties [ELE:CN, $1.66, $408.3M]: The story centers on their announced merger to create a new mid-tier player. The deal is financially backstopped and strategically driven by Tether, the world's leading stablecoin company, which is set to become the largest shareholder with up to a 33% stake. Tether is described as "extraordinarily bullish hard assets" and views this as their entry into the royalty space.

• Empress Royalty [$82.3M]: Empress was set up to fill a specific gap in the market: providing financing in sub-$25 million ticket sizes that larger companies have grown too big to service. Its strategy is to act as a direct financier, creating new royalties and streams by investing in near-term producers for development or expansion, leveraging its team's structured finance expertise.

Portfolio & Risk Management: Balancing Geography and Structure

Each company has constructed its portfolio to manage risk and optimize returns through different approaches to geography and asset structure.

• Franco-Nevada: Manages risk with a balanced portfolio of "half streams, half royalties" to capture both "gold price optionality" and "resource optionality". Influenced by global deglobalization, the company has a long-term objective to orient its portfolio more towards "good countries".

• Wheaton Precious Metals: Employs a unique "100% streaming model" on long-life base metal mines, giving it a reserve and resource profile of nearly 60 years. It takes a global, risk-adjusted approach, comfortable investing in many jurisdictions as long as the risk is "captured in terms of the expected returns".

• Royal Gold: Manages risk through diversification. While recent deals add exposure to Ecuador and Zambia, almost 40% of its NAV remains in the US and Canada. No single asset accounts for more than 12% of NAV, preventing concentration risk.

• OR Royalties: Uses low jurisdictional risk as a key differentiator, with 80% of its NAV in Canada, the US, and Australia. It also has the "highest cash margin" at 97% due to its royalty-centric portfolio, insulating it from cost inflation.

• Gold Royalty Corp.: Also focuses on low political risk, with over 80% of its portfolio in Nevada, Quebec, and Ontario. Its portfolio of over 250 royalties is all "fully bought and paid for" with no future capital calls, de-risking its pipeline.

• EMX & Elemental Altus: The merger creates a significant global portfolio with over 200 royalties in roughly 20 countries, which the CEO says "looks like something a major would have". The portfolio is diversified by commodity, with current revenues at 67% precious metals and 33% base metals.

• Empress Royalty: Manages risk through a unique "pure gold and silver" focus, believing precious metals offer a premium to investors. It has a global focus and will transact in any mining-friendly region where its team has experience, resulting in a diverse portfolio across Mexico, Peru, South Africa, and Mozambique.

Key Assets & Growth Drivers: The Engines of Future Returns

A mix of cornerstone assets and deep development pipelines underpins the companies' growth outlooks.

• Wheaton Precious Metals: Claims the "highest growth rate," targeting 40% growth over five years on its mission to reach one million GEOs annually. This is driven by its flagship Salobo stream and a pipeline including Plat Reef, Goose (with B2Gold [BTO:CN, $4.40, $5.8B]), and Blackwater (with Artemis Gold [ARTG:CN, $23.95, $5.5B]).

• Franco-Nevada: Has the single largest catalyst in the potential restart of the Cobre Panama mine [+150,000 GEOs/year]. Long-term growth is secured by recent deals on generational assets like Yanacocha (with Newmont [NEM:US, $79.36, $87.2B]) and Arthur Gold (with AngloGold Ashanti plc [AU:US, $67.10, $33.9B]).

• Royal Gold: Future growth is tied to the development pipeline acquired from Sandstorm, particularly Hod Maden (SSR Mining), Mara, and Plat Reef. A critical achievement is the life extension of its cornerstone Mount Milligan mine to 2045 with operator Centerra Gold Inc. [CG:CN, $9.24, $1.9B].

• OR Royalties: Is anchored by its cornerstone 5% NSR on Canadian Malartic, the "most valuable royalty out there," operated by Agnico Eagle Mines Limited [AEM:CN, $153.76, $77.2B]. This asset underpins a forecast of 40% organic growth by 2029 with "no development risk".

• Gold Royalty Corp.: Projects "peer-leading" growth to 23,000-28,000 GEOs by 2029. This is driven by a broad portfolio including a copper stream on the Vares mie (now operated by DPM Metals Inc. [formerly Dundee Precious Metals] [DPM:CN, $21.46, $4.8B]) and foundational royalties on Canadian Malartic and the REN project, the extension of Barrick's Gold Strike mine.

• EMX & Elemental Altus: Growth will be driven by a robust combined portfolio of 4-5 cornerstone assets. Key assets include a now-combined 1.3% NSR on the massive Casarones mine (Lundin) in South America (paying over $15M/year) and the Timok (DPM) copper-gold royalty in Europe, described as "one of the most exciting royalties within the entire portfolio".

• Empress Royalty: Growth is driven by the cash flow from its four initial investments, which it is now reinvesting. Its assets are already demonstrating strong returns, such as a $5M investment in the Tahuehueto silver mine now yielding $6.9M annually, and a $3M investment in the Manica gold mine that has already returned $6M and continues to pay.

Financial Priorities & Capital Allocation: Deploying Capital in a Bull Market

Each company's approach to capital allocation reflects its strategic maturity and financial position.

• Franco-Nevada: With cash flow approaching $1.5 billion per year, its priority is deploying capital only into deals that meet its strict criteria for profitable growth.

• Wheaton Precious Metals: Prioritizes "accretive, well-structured acquisitions," investing based on a conservative "backwards curve" for commodity prices, not its own bullish outlook.

• Royal Gold: Priorities are ranked: 1) new investments, 2) debt repayment (projected at ~$1.2B post-merger), and 3) maintaining its 24-year history of dividend increases.

• OR Royalties: Has zero gross debt and is accumulating cash. Priorities are deploying capital into new assets, increasing the dividend, and using its share buyback program.

• Gold Royalty Corp.: Is focused on its balance sheet, expecting to be net debt-free by the end of 2026, after which it will be in a position to return capital to shareholders.

• EMX & Elemental Altus: The primary financial driver is the merger, designed to achieve a significant P/NAV re-rate. This is supported by a new $100 million investment from Tether, ensuring the combined entity has up to $250 million in firepower for future acquisitions.

• Empress Royalty: Having proven its model, the company's key focus is now to deploy its growing internal cash flow and a $20 million available debt facility to diversify its portfolio by investing in more high-quality, small-scale assets.

Bullish Takeaways

• Wheaton Precious Metals: Investors are buying into the sector's quality leader, which offers the highest organic growth profile (40% in 5 years) driven by a de-risked portfolio of long-life streams, all while maintaining a disciplined, risk-adjusted approach to new investments that prioritizes accretive deals over sheer scale.

• Franco-Nevada: The investment thesis is anchored by a proven, profitable growth strategy and the single most significant catalyst in the sector: the potential restart of the Cobre Panama mine, which could boost production by 50% by 2029, offering immense, asymmetric upside that is not fully reflected in current guidance.

• Royal Gold: The "transformational" acquisition of Sandstorm has created a deeply diversified portfolio with a world-class development pipeline (Hod Maden, Mara, Plat Reef) that, if successfully executed, will drive significant, long-term NAV and cash flow accretion for shareholders.

• OR Royalties: An investment offers a compelling combination of safety and growth, with a peer-leading 40% organic growth profile by 2029 that is fully funded and de-risked, anchored by a world-class cornerstone asset (Canadian Malartic) in a Tier-1 jurisdiction.

• Gold Royalty Corp.: Investors gain exposure to a high-growth, small-cap consolidator with a peer-leading volume growth profile and a vast, de-risked portfolio of 250 royalties that provides significant free optionality from over $200M in annual partner-funded exploration.

• EMX & Elemental Altus: The merger creates a newly-scaled mid-tier company trading at a significant discount to peers (~1.0x P/NAV vs. ~2.0x), offering a clear catalyst for a valuation re-rate driven by increased liquidity and ETF inclusion. This is further de-risked and amplified by the financial backing of Tether, a major new strategic shareholder providing significant firepower for future acquisitions.

• Empress Royalty: An investment offers exposure to a pure-play precious metals vehicle that has proven its unique model of financing near-term producers in the underserved sub-$25 million market, generating substantial and immediate cash flow returns that position it as an undervalued growth story as it deploys its growing capital.