The Royalty & Streaming Titans: Record Deals Signal a New Era

Wheaton Precious Metals and Royal Gold used 2025–26 to reshape the streaming sector with landmark acquisitions — and they're just getting started.

MINING FORUM EUROPE 2026, ZÜRICH - If the last eighteen months proved anything about the precious metals streaming and royalty model, it is that these companies are no longer niche financiers operating at the margins of the mining industry. They are becoming its center of gravity. At Mining Forum Europe 2026, both Wheaton Precious Metals and Royal Gold presented portfolios that have been fundamentally transformed by a wave of dealmaking unprecedented in the sector’s 22-year history.

Wheaton completed the largest precious metals streaming transaction ever in February 2026, a deal with BHP that added exposure to one of the world’s premier mining houses. That single transaction underscored a broader shift: major diversified miners that had historically avoided streaming are now embracing it as a financing tool, opening a universe of Tier 1 assets that were previously off-limits to the royalty sector.

Royal Gold’s Double Acquisition

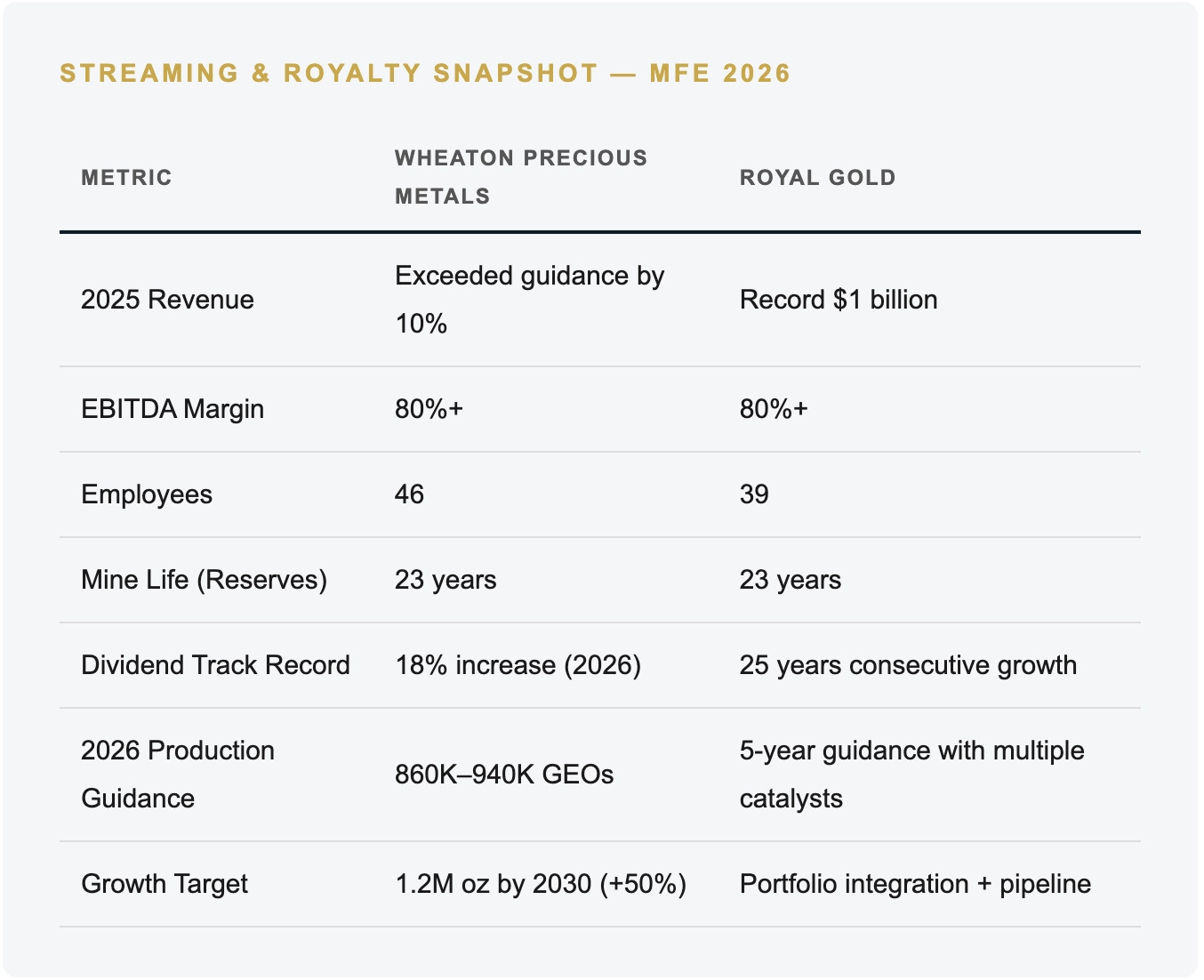

Royal Gold, for its part, executed the largest corporate acquisition in the streaming and royalty sector’s history, absorbing both Sandstorm Gold and Horizon Copper in deals totaling $5.3 billion over just six months. The combined portfolio now spans more than 360 investments globally, with 80 producing properties, 30 in development, and over 250 in earlier stages. The company remains the only US-domiciled streaming and royalty business — a structural advantage for index inclusion and US institutional flows.

The Sandstorm integration is strategically elegant due to portfolio complementarity. Royal Gold’s legacy strength was near-term, cash-flowing assets. Sandstorm brought a longer-dated pipeline of development-stage optionality. Blended together, the result is a company with 23 years of mine life from reserves alone, 95% of consensus NAV from precious metals, and 70% of NAV from the Americas.

“Our model requires time. Excess returns emerge over time if you’re patient.” — Dan Breeze, Royal Gold

Why the Model Wins in This Cycle

The streaming model’s power becomes especially visible when metal prices rise. Unlike operating miners, whose costs tend to inflate alongside revenues, streamers capture the price upside almost entirely as margin. Both Wheaton and Royal Gold reported EBITDA margins exceeding 80%, a figure that would be extraordinary in any industry, let alone one involving physical commodity extraction.

Wheaton runs the entire business with 46 employees. Royal Gold manages a $22 billion market cap with 39 people and cash G&A costs of just 4% of revenue. The operational leverage is staggering: when gold rises $100 an ounce, the incremental cash flow drops almost entirely to the bottom line.

The Growth Pipeline Is Deep

Wheaton’s forward production profile tells a compelling story. From roughly 800,000 gold-equivalent ounces in 2025, the company is targeting 1.2 million by 2030 — a 50% increase driven entirely by expansions and new project ramp-ups within the existing portfolio. Key catalysts include first production at Kona and Kermu (late 2026), El Domo (mid-2027), and a potential throughput increase at Salobo, where Vale is evaluating a six-million-tonne-per-annum expansion.

The Antamina stream alone could prove generational. The mine’s reserve life officially runs to 2038, but management views the asset as potentially operating for 40 to 60 years with underground extensions — the kind of multi-decade exposure that compounds quietly in the background.

Royal Gold’s growth, meanwhile, is more distributed. The combined portfolio now contains dozens of development-stage assets that could convert to cash-flowing streams over the coming decade, with the company actively evaluating roughly 15 opportunities, mostly in the $300–500 million range. After years of limited deal flow in Australia, the market there is opening up following Royal Gold’s KGL reservoir transaction — the first Australian stream.

What This Means for Investors

The overarching message from both presentations was that the streaming sector has entered a structural growth phase. The BHP deal signaled to the world’s largest miners that streaming is no longer a tool of last resort for junior developers. It is a legitimate, cost-effective mine financing option for anyone. That single shift in perception could unlock a pipeline of Tier 1 opportunities that the sector has been pursuing for over a decade.

For investors looking for leveraged exposure to rising precious metals prices without the cost inflation, permitting risk, or operational complexity of running mines, royalty and streaming companies are in a strong position. As Wheaton noted in Zurich: “All streams are not created equal.” In this cycle, the best ones are being created at record scale.