Where is New Silver Supply Going to Come From?

Silver poised for sixth straight year of deficit

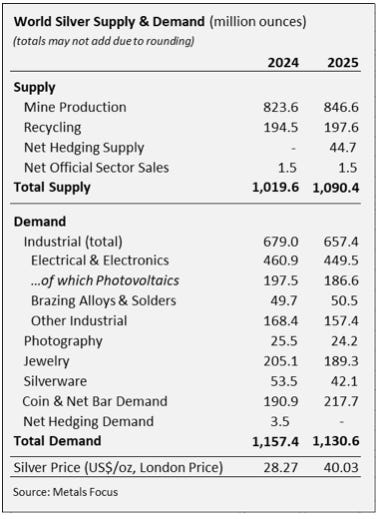

The silver market was in deficit in 2025 for the fifth consecutive year, a situation that is not projected to reverse any time soon.

The World Silver Survey, which was prepared for the Silver Institute by Metals Focus, was released earlier this month.

Total silver demand fell by 2% in 2025 to 1.13 billion ounces with a 14% jump in coin and bar demand almost offsetting a 3% slide in industrial demand, an 8% drop in jewellery fabrication and a 21% slump in silverware demand.

Total supply last year was 1.09Boz, with global silver mine production rising by 3% to 846.6 million ounces.

The gains came from higher by-product output from copper operations in Peru, the ramp-up of Polymetal JSC’s Prognoz mine in Russia and smaller gains were from Chinese and Moroccan operations, which were partly offset by lower output from operations in Mexico and a decline in Indonesia.

North American output fell by 3% to a 10-year low, while Central and South American production rose by 5%.

Recycling rose by 2% to a 12-year high of 197.6Moz.

Silver demand in 2026 is forecast to fall by 2% to 1.11Moz, with a further rise in coin and bar demand to be offset by falls in jewellery, silverware and industrial demand.

Mine production is expected to remain flat this year.

As a result, the structural market deficit is projected to widen to 46.3Moz in 2026, which translates into a cumulative stock drawdown of 765Moz since 2021.

“This, along with renewed ETP demand and ongoing US tariff uncertainty, leaves the market vulnerable to another liquidity squeeze,” Metals Focus said.

“In turn, this suggests that heightened volatility and further price gains appear likely in 2026.”

While the Iran War complicated the short-term outlook, the report concluded that the broader macroeconomic and geopolitical backdrop remained supportive for silver prices

Producers bullish

Silver prices reached record highs of more than US$120 an ounce in January but are sitting at around US$75/oz today.

While prices have been volatile, silver producers attending this month’s Mining Forum Europe in Zürich were optimistic about the demand outlook.

“Silver is a very complex story, much more complex than gold, because silver has two uses,” Pan American Silver Corp (NYSE: PAAS) president and CEO Michael Steinmann told the event.

“The use right now on the industrial side is growing so fast that we are already at about 65% of the world’s silver production that is used up, and you can imagine with further electrification – not only with clean energy production – but self-driving cars, data centres, AI, the use of silver is increasing very, very fast.”

The silver market is expected to remain in deficit until at least 2030.

“We know there’s no significant silver coming online, and that deficit is going to prevail for quite some time,” First Majestic Silver Corp (NYSE/TSX: AG) president and chief corporate development officer Mani Alkhafaji said during the forum.

“There are new industries that are coming in the market that’s not being talked about.

“We just came from a recent conference and there’s discussion about the AI data centres. On average, a data centre consumes 6.6 tonnes of silver and that’s a significant number that’s not being replaced by any new supply hitting the market.”

New supply

Steinmann pointed to the difficulty in bringing on new silver supply.

“75% of the production comes as a byproduct from copper production, and copper is already at an all-time high, nearly, and there’s not many big copper mines coming on in the next few years, so hence not much more silver production,” he said.

Steinmann said Pan American’s La Colorada Skarn project in Mexico and the potential restart of the Escobal mine in Guatemala was the only meaningful future additions to production.

A March revised preliminary economic assessment for the La Colorada skarn expansion returned capital costs of US$1.9 billion for a 37-year operation producing 15.8Moz of silver and 239,000t of zinc per year in the first five years, in addition to the 3.3Moz of silver and 6000t of zinc per year produced by the La Colorada vein mine.

Discovery Silver Corp (TSX: DSV) owns the world’s largest undeveloped silver deposit, Cordero in Mexico, which has been stalled by permitting delays.

Discovery senior vice president, investor relations Mark Utting said the company was encouraged by Silver Tiger Metals Inc (TSXV: SLVR) recently receiving a permit for its El Tigre silver development in Mexico.

“We know that the project was reviewed with the president in late January as one of several key projects for the country. We understand it was basically green-lighted at the executive level,” he said.

“It is our understanding, basically, we’re looking at a government administration exercise, so when we say that we are confident we’re going to be permitted very soon, that is the basis of that optimism.”

Discovery will then spend around six months updating the economics for the 14Moz per year project and could start construction by late 2026.

These days, 70% of Coeur Mining’s (NYSE: CDE) revenue comes from gold, but the company is advancing the Silvertip polymetallic project in British Columbia.

Coeur SVP and chief financial officer Tom Whelan said the company had just completed a PEA, which would be presented to the board in May ahead of a decision on whether to move to a prefeasibility study.

“I don’t want to get ahead of the board, but obviously with this higher silver price environment, all of the work that we’ve done, we’re starting to get pretty excited,” he said.

“Just to give you a sense of the order of magnitude of what that could look like, Silvertip’s an 11 million tonne resource at 300 grams silver. If you take 2000-3000t a day, that’s 6-8 million more ounces of silver.”

Also a gold-silver producer, Kingsgate Consolidated (ASX: KCN) is dusting off plans for its 61Moz Nueva Esperanza silver development in Chile.

“It is easily one of the largest underdeveloped silver projects in South America, I think, in fact, probably globally,” Kingsgate managing director Jamie Gibson said.

“I think if you look at the size of the resource, it’s probably in the world’s top 10.

“In fact, Kinross had this in the late ‘90s and it was the largest silver mine in the world. I think those guys got something like 35-40 million ounces out of it in about 13 months, so we know it’s got scale.”

Kingsgate has appointed new consultants and will update the 2016 PFS.

Hecla Mining (NYSE: HL) is already the largest silver producer in the US and Canada and will look at the restart of Midas in Nevada in the medium-term.

“The story is we’ve got a nearly fully permitted 1200 tons per day mill, tailings infrastructure, surface facilities, utilities in place, and our 2025 exploration program was pretty exciting. It identified a couple of new structures, new veins, both very high-grade,” Hecla CEO Rob Krcmarov said.

“The path from here is really aggressive exploration 2026. If that continues to pan out, resource definition and technical studies in the next year or two, then a go decision and production perhaps 3-4 years beyond that, so realistically, potentially an operating mine in, let’s call it the next five years or so.”

Other growth

Juniors presenting in Zürich also outlined silver growth plans.

Aya Gold & Silver (TSX: AYA) is growing silver production at Zgounder in Morocco from 5Moz last year to nearly 7Moz this year and is aiming to reach 43Moz of silver equivalent by 2029 via the development of its second mine, Boumadine.

Americas Gold & Silver Corp (TSX: USA) has flagged a 30% increase in silver production in Nevada this year from 2.65Moz to 3.2-3.6Moz.

Avino Silver & Gold Mines (NYSE American: ASM) president and CEO David Wolfin spoke of the company’s plans to go from one producing mine in Mexico to three operations by 2028, with production to rise from around 2.5Moz per year to 8-10Moz.

Kuya Silver Corp (CSE: KUYA) is planning to increase production from Bethania in Peru this year to 1.5Moz and double production by 2028.