Taking the Pulse of Mining Forum Europe 2026 - A Roundup of the Key Topics & Trends

Notes from three days on the floor, across five keynotes and a panel discussion, sixty-three company presentations, and 70 mining issuers.

Gold closed the first day of the forum above $4,000 for the tenth consecutive quarter of record prints. Silver was changing hands a few dollars off its February highs. The Park Hyatt Zürich, as you would expect, was louder than last year, fuller than last year, and even better dressed if that’s possible for Zürich. What was not louder, and what struck me most across three days of panels and sixty-something company presentations, was the euphoria. There wasn’t any.

Let me try to pull the signals out of the noise after sitting through the keynotes, the capital markets panel, and clocking every issuer presentation I could get to. Below are the themes that showed up again and again, the data points worth filing, and the moments I think actually mattered for the industry.

The de facto gold standard nobody is announcing

If you want one idea to carry out of Mining Forum Europe 2026, it is this. The freezing of Russia’s foreign exchange reserves in 2022 was a structural break, not a headline. Central banks outside the G7 have been buying gold relentlessly ever since, and they have not stopped. Nicky Shiels of MKS Pamp framed the thesis with her “three Ds”: debased, diversify, de-dollarize. The numbers are hard to argue with.

Central banks now hold roughly 1.1 billion ounces of gold, about ten times annual primary mine supply and ten times the global ETF pile.

Emerging market central banks would need to buy about 22,000 tons to catch up with developed market gold-to-forex ratios. That is seven years of total mine output.

Turkey sold 120 tons in Q1 and still has not dented its accumulation trend. France repatriated gold from New York to Paris. Nobody in the room thought that was a coincidence.

Gold has a higher market value on central bank balance sheets than US Treasury holdings do. It is a larger share of the world's official reserves than the euro.

Chris Wood, Jefferies macro strategist, put it plainly in a packed capital markets keynote. We are mid-cycle, not late-cycle, because we have done all of this without a meaningful dollar depreciation cycle. When the dollar finally rolls over, the second leg begins. His target methodology yields $6,800 per ounce on a disposable income basis and roughly $13,000 per ounce against US M2.

Zoltan Poszar had some parallel and even contrary insights, but we can’t share them because it was a Chatham House Rules presentation.

Discipline is the tell, and it looks a lot like fear

The 2011 cycle ended with mega mergers, bad projects financed at bad prices, and a lot of people who should have known better building expensive mines into a falling market. You can spend a whole career unlearning that, and miners are doing it. Neil Adshead of Centerra / Cupel Advisory was blunt on the risks of “capital misallocation” in his keynote presentation and in the panel discussion. Miners do not believe the current gold price. They are running reserves at prices close to half of spot. Boards are sitting on $10 million to $30 million in paper gains on personal shareholdings. They do not want to commit $3 billion to $5 billion to a project that pays back in ten years.

You can frame that as discipline or you can frame it as fear. Either way, the effect is the same. The North American gold sector is projected to throw off about $35 billion in free cash flow in 2026. Average balance sheets across the majors are expected to cross $42 billion by year end. Very little of that cash is going into new mines. Most of it is going to dividends, buybacks, and selective M&A of things already built.

Euphoria builds tops. The absence of euphoria is why the top is not here yet.

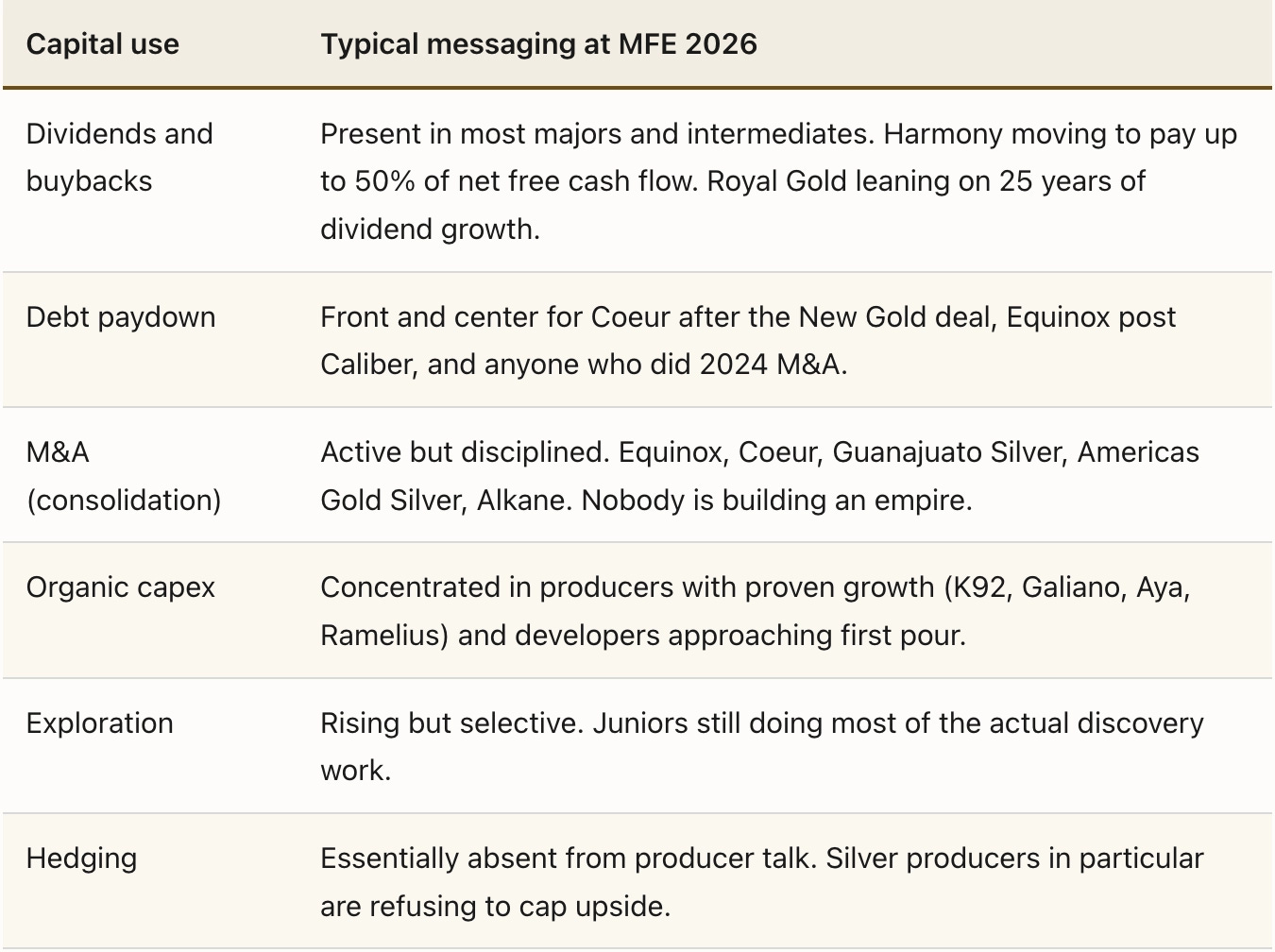

Capital allocation, by the numbers

Across the sixty-three company presentations I tracked, the posture was remarkably uniform. Here is the rough distribution of how producers are talking about their cash.

The institutional void

If central banks are the buyer of last resort, US institutional investors are the buyer of never. Shiels walked us through the math. Retail and family office allocations to gold are running under 1% of portfolios in the US, down from the 2011 peak near 1.6%. Generalist mutual fund complexes have vanishingly small positions. Wood said that when he was on the sell side covering the sector, most generalist portfolio managers in America knew only two gold mining stocks: Newmont and Barrick; the sum total of their sector knowledge.

Rather than accusing capital allocators of apathy, it can be put down to simple structural exclusion after years in the doldrums and on the margins of the big stories in the markets. The eventual reallocation, when it comes, is unlikely to be a gentle drift. 60/40 portfolios cannot add 2% to gold without moving GDX several multiples higher from here, because the float is not there. Retail got the memo in Q1. Silver ran from around $60 to $120 and back to $60 in what one panelist, not unfairly, called meme stock behavior, with leverage as high as 1 to 100 on CFDs in some jurisdictions. That was retail front running a move that has not started in institutional allocations.

The ETF and options flow data I reviewed during breaks support the same conclusion. US investors are still dramatically underweight an asset class that has already doubled. It very much reinforces that we have a mid-cycle mood.

Canada ate the koala

A very entertaining keynote at the forum was John Forward of Lowell Resources on the ASX-to-TSX valuation gap. I am going to give him the space he deserves because the thesis is so clean and the numbers are so striking.

For most of the last decade, Australian juniors ran circles around Canadian ones. Post 2024, that reversed and the reasons are mechanical, not ideological.

Canadian juniors can “hibernate” on roughly $100,000 in overhead (audit, insurance, listing fees). Australian juniors burn closer to $1 million before anyone does anything useful. That drives relentless capital raising, which drives relentless equity dilution.

Across twenty intermediate gold producers he tracked, ASX-listed names issued roughly seven times as many shares as their TSX peers over the same period.

Flow-through shares still fund about 70% of Canadian exploration. The Australian equivalent ended in 2024. There is simply no parallel capital channel Down Under.

On a per-production-ounce basis, TSX intermediate golds trade around $22,000 per ounce of EV. ASX peers trade around $12,000. Over the twelve months to April 2025, TSX EV per ounce rose about 2.3x, and ASX about 1.7x. The gap is widening, not closing.

In 2026, John expects Canadian junior fundraising to exceed Australian fundraising for the first time in years.

“The Canadian brown bear hibernates better than the Australian koala. And the koala isn’t actually a bear.”

Australians are spendthrifts. Canadians are misers with share capital. If you are looking for leverage into the next leg, you want misers, but never count the Aussies out of any innovation drive as the sector continues to boom (visit Perth’s golden triangle to see a gigantic mining wealth effect in play).

Juniors find, majors buy

The capital misallocation discussion doubled as a quiet commercial for Centerra’s exploration portfolio model. Neil Adshead now manages a roughly $25 million junior investment book for Centerra. Two years in, it is worth north of $40 million, and the major has optioned three projects into its own drill program out of that pool. Agnico Eagle runs something similar at seventy names. The lesson most of the room took from this is that majors are bad at greenfield discovery and juniors are good at it. The actual lesson is less dramatic: Majors are bad at drilling holes because they have too much money and too many meetings. Juniors are good at drilling holes because if they do not drill, they die.

Expect this model to spread as the bigger royalty and streaming names expand exploration investment mandates. Expect more majors to anchor juniors with minority positions and offtake-style first rights. For juniors sitting on a classy North American project, the prospects for a bidding war are outstanding.

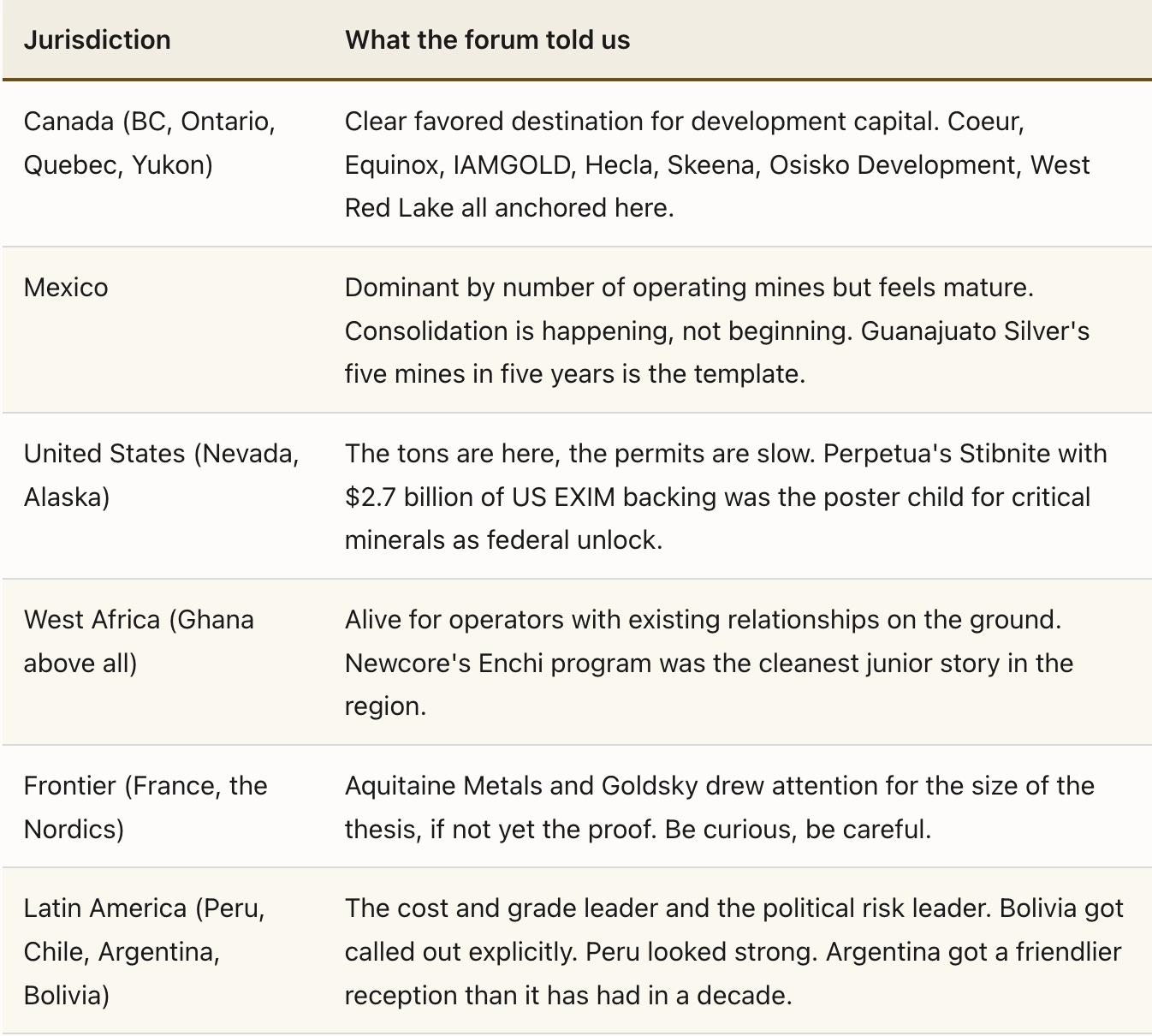

Permitting is the gate; jurisdiction is the key

For company presentations, the single most common constraint discussed, far ahead of labor, power, or capex inflation, was permitting, which remains the gate. Everything else is geology and cost accounting. The map that emerged was roughly this:

What wasn’t said

For a forum this large and representative of the mining investment space, some of the silences were as useful as the statements.

Almost nobody talked about hedging. Producers are leaving upside open.

Nobody pitched mega capex. Greenfield growth was framed as optionality, not commitment.

Nobody defended cost inflation. They described it, they countered it with operational specifics, they did not pretend it was over.

Nobody defended single jurisdiction concentration as a feature. Those that had it apologized for it implicitly by offering exploration optionality elsewhere.

Very few developers were bold enough to say their permits guaranteed. Those that could (Liberty Gold, Paramount’s Grassy Mountain, Osisko Development’s Caribou) wore it like a medal.

Macro headwinds worth tracking

Wood made the case that the right tail risk to a gold target near $7,000 is not the Fed and not the dollar but the US Treasury. With 84.9% of US Treasury issuance in the last year inside one year maturities, and net interest plus entitlements running at 92.7% of federal receipts, the Fed does not have the room to stay hawkish even with a hawk (Walsh) now at the helm. Formal yield curve control is unlikely, but financial repression via negative real rates, credit controls, and selective regulation is very likely. Both outcomes are gold positive.

On the AI complex, Chris argued the hyperscalers have become the capital expenditure whales of the US economy. Capex as a share of operating cash flow at the four biggest US hyperscalers is running around 84%. He thinks the large language models end up looking like a commodity industry with airline style economics rather than winner takes all. If he is right, the unwind of that capex cycle lands sometime in the next eighteen months and it lands hard on the S&P, which has made gold miners look small even as they have doubled. A hyperscaler crack is the shock that forces the institutional reallocation I described above.

Memorable lines from the floor

“Gold miners don’t believe in the current gold price.”

Neil Adshead“Aussies are spendthrifts. Canadians are misers with share capital.”

John Forwood“Silver became almost a meme stock. People putting down 1 to 100 leverage.”

Nikki Shiels“Central banks now own more gold at current market price than US Treasury bonds.”

Chris Wood“Once it’s up and running, it’s wonderful. You can keep levying more and more tax and royalty on it.”

Neil Adshead, on why the jurisdictional risk premium is going to widen, not narrow.

Bottom line

Mining Forum Europe 2026 was not yet the top. The top looks like confidence, capex commitments, and coverage. This forum was careful, disciplined, and underpositioned. Central banks are buying gold as a monetary reset in all but name. US institutions are still outside. Producers are returning cash rather than building. Canadian juniors have quietly become the best structured leverage into the next leg. Juniors still do the discovery. Majors will pay up for it on the other side. Permitting is the gate, jurisdiction is the key, and the people who get both right in Canada, Nevada, Alaska, and select pockets of West Africa will own the next five years.

Mid-cycle. Not late cycle. The koala needs to find more eucalyptus.